How much cash should you keep in savings accounts? At a glance

- What do I need to know? Saving a portion of your wealth in high-interest accounts and Cash ISAs can provide stability and easy access to your cash while earning interest, depending on the accounts you open.

- What does it mean for me? It’s important to consider how much money you keep in cash savings to balance growth, access, and protection against loss.

- Why does it matter? A balanced savings and investment portfolio could give you more options to navigate uncertainties and align your growth according to your financial goals.

Saving money in high-interest accounts and Cash Individual Savings Accounts (ISAs) can provide a relatively low-risk way to grow your wealth, with the latter also offering tax-free interest.

Instant access accounts in particular can also keep your money readily available when new opportunities arise. But how much should you keep in savings?

And how can you balance a significant savings portfolio alongside investments such as venture capital and Stocks and Shares ISAs, which could result in higher returns but involve greater risk?

In this guide, you’ll learn how much to keep in savings to prioritise access, growth, and protection. You’ll also learn about the role cash savings can play within your wider wealth strategy.

How much should you keep in savings?

There’s no golden rule for how much of your wealth you should hold in cash. And how much you keep in savings might change throughout your life, depending on your circumstances. You can speak to a qualified financial adviser to discuss your personal circumstances and how to structure your wealth in line with your priorities.

For example, you may wish to hold a lower proportion of your wealth in cash during your peak earning years, if faster growth is a priority for you. This could help you to meet your goals of growing your wealth for retirement or building generational wealth.

But it could also mean you take on greater risk as a result. As you near retirement, you might convert a greater proportion of your wealth into cash, giving you the freedom to enjoy your golden years. You may also choose to use cash to pass on wealth to loved ones early by using gifting allowances, or the seven-year rule.

In some cases, this can make gifting money simpler, as there are additional tax rules to consider when you give away certain assets such as property.

Balancing access and growth

Accessible cash savings can play an important role when it comes to growing, enjoying, and sharing your wealth with your loved ones. Other types of investment, such as venture capital or private equity investing, can often provide much greater growth potential than high interest savings accounts.

But the unpredictability of those investments mean you could experience a higher risk of losing the money you put in. They are also long-term investments, making your money difficult to access should you need it. investments, making your money difficult to access should you need it.

In general, concentrating too much of your portfolio in higher-risk assets can expose your overall wealth to greater instability. So, it’s essential to balance your risk appetite (how much you’re prepared to lose) with growth potential.

Combining savings account types for greater balance

By contrast, high-interest Instant Access savings accounts can provide a secure and accessible method to grow your funds. They give you the freedom to pursue emerging investment opportunities, without sacrificing the ability to earn interest.

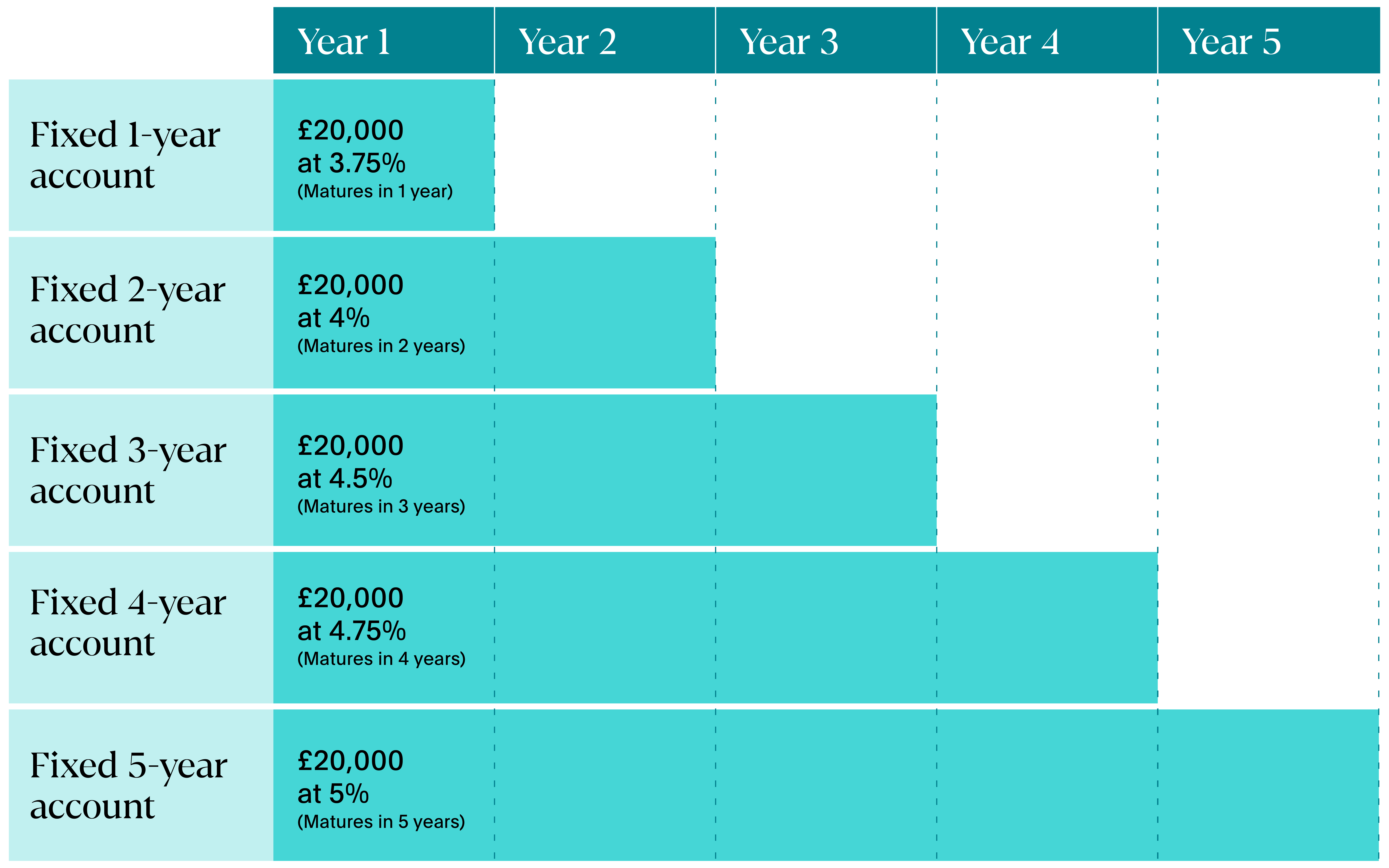

Alternatively, you might want to commit some of your cash to Fixed Rate savings accounts, which typically deliver higher interest rates in exchange for locking your money away for a set period.

Using a range of fixed-term accounts with different maturity dates can help you create a laddered savings approach.

You can use a savings platform like Flagstone to build a portfolio of account types, letting you combine the benefits of each in one place.

Protecting cash savings

Cash savings can build wealth through interest and provide flexibility for your finances, especially when you save money at scale.

But how you save is just as important as what you put aside, and some approaches offer greater protection against loss than others.

Inflation

If inflation outpaces your interest rate, you could risk losing purchasing power. So, leaving your cash sitting in low-interest savings accounts or current accounts could mean it loses value when you come to spend or reinvest it.

Prioritising high-interest savings accounts, and Cash ISAs which offer tax-free interest, can help you preserve and increase the value of your cash in an unpredictable economic environment.

FSCS protection

It’s important to consider whether you benefit from Financial Services Compensation Scheme (FSCS) protection when you hold a large portion of your portfolio in cash. If you hold too much in a single savings account, you risk losing some of your wealth if the unexpected happens.

In the UK, FSCS protection ensures that eligible deposits are reimbursed up to £120,000 per individual, per financial institution if your provider goes out of business. Joint accounts are protected up to £240,000 per financial institution.

So, spreading your cash between different accounts, with separate providers, can increase your protection because you’re placing deposits with unique financial institutions.

The three types of savings accounts

Not all savings accounts are the same. And you can distribute your cash between different types of savings accounts to balance access and returns at different stages of your life.

There are three main types of savings accounts:

- Instant Access accounts: give you the flexibility to access your money as and when you need it but come with slightly lower, variable interest rates.

- Notice accounts: offer slightly higher returns when you agree to a short notice period, balancing access with growth and variable interest rates.

- Fixed Rate accounts: typically provide higher, predictable returns when you lock away your cash for a set period, growing your earnings at a fixed rate on funds you don’t need in the short term.

Frequently asked questions about savings accounts

Is it bad to keep too much money in savings?

How much money you keep in savings will depend on your financial goals. But it can be beneficial to keep some cash in instant access savings accounts so you can respond to investment opportunities as they arise.

Holding too much cash in a single savings account can expose your money to risk if the amount exceeds the FSCS protection limit. This is why savers are increasingly opening multiple savings accounts through platforms like Flagstone.

Should I keep savings in one account or spread them out?

Depending on the size of your balance, you may want to spread your cash between multiple accounts with different financial institutions to diversify your portfolio and help protect your funds.

This is because, if your bank goes out of business, the FSCS protects deposits up to £120,000 per individual, per financial institution.

Should you use fixed rate savings accounts?

Fixed rate savings accounts can be a useful addition to a savings portfolio as they typically offer higher interest rates in exchange for locking your cash away for a set amount of time.

When you open a fixed rate account, you’ll know how much you’ll earn at the end of the term. This can help your financial planning by giving you a more predictable return.

How often should you review your savings?

There is no strict guidance on how often you should review your savings, and you can do so as frequently as needed.

But reviewing your savings regularly can help you reassess whether you’re on track to meet your financial goals.

What should you do after selling a business or receiving a large lump sum?

How you structure your wealth when you receive a significant lump sum is your decision, but your choices can impact your future finances.

Depending on how and when you acquired the money, you may have a significant amount of tax to pay. It’s important to speak with a financial adviser to receive guidance based on your personal circumstances.

Balancing growth, protection, and access with cash savings

The right amount of money for you to keep in cash savings will depend on your personal circumstances. In general, this means creating the best balance between access, protection, and your appetite for risk.

Cash savings can increase your options when it comes to pursuing new investment opportunities, or even sharing your wealth with loved ones.

But it’s important to prioritise FSCS protection and high interest rates to protect your money and its purchasing power.

And maximising tax-free savings allowances such as the annual ISA limit can further develop your savings strategy, shielding your wealth from unnecessary costs.

Manage a high-interest savings portfolio with Flagstone

Flagstone’s savings platform gives you access to high-interest savings accounts and Cash ISAs from 65+ banks with a minimum deposit of £10,000.

All in one place, with one password.