R&D tax relief: at a glance

• What do I need to know? Research and Development (R&D) tax relief is a government incentive designed to encourage UK businesses to invest in innovation by reducing the tax they owe.

• What does it mean for me? HMRC applies the relief as a reduction to your Corporation Tax bill or as a cash payment. Either way, it might mean more money stays in your business.

• Why does it matter? This additional cash can support growth, cover costs, or fund your next innovation. A business savings account can help you protect and grow that money until you need it.

The latest government data shows that UK businesses claimed an estimated £7.6bn in Research and Development (R&D) tax relief in the 2023 to 2024 tax year.

Data for 2024 to 2025, the first year under the new merged scheme, isn't yet available – but the relief remains open. If your business is investing in innovation, you may be eligible too.

R&D tax relief can cut the cost of developing new products, processes, or services. And a successful claim means you could keep more cash in your business to support your goals.

In this guide, you'll learn about R&D tax relief, how it works, and how you can benefit from it.

What are R&D tax credits?

R&D tax credits are a government incentive designed to encourage technological innovation and reward businesses taking risks to develop new products and services.

Research and development includes work that seeks an advance in science or technology by resolving scientific or technological uncertainty that a professional in the field couldn’t readily resolve. This can include any industry, not just lab-based research businesses.

Profitable businesses can claim a reduction on their Corporation Tax bill for earnings generated through cutting-edge research and development projects. Businesses that undertake similar projects but don't generate significant profits or make a loss may instead receive a cash payment from HMRC.

You can check the details on the GOV.UK website to find out whether your projects qualify for relief and how to apply.

How does R&D tax relief work?

There are specific criteria for which businesses can qualify. What you can claim depends on the size of your business and your existing tax year finances.

Any UK company liable for Corporation Tax and investing in qualifying R&D projects can claim R&D tax relief. Some loss-making SMEs may also qualify for more generous support, depending on their size and turnover (more on this below).

How much you can claim depends on which regime applies to your accounting period. If your accounting period started on or before 01 April 2024, you can find details about the relief available to your business on the GOV.UK website.

HMRC introduced a new structure for R&D tax relief for accounting periods starting on or after 01 April 2024. There are now two regimes to be aware of – the merged R&D scheme and enhanced R&D intensive support (ERIS).

The merged R&D scheme

The merged scheme replaced the two separate schemes that previously applied to SMEs and large companies. Now company size no longer determines which scheme you use.

Under the merged scheme, you receive a credit worth 20% of your qualifying R&D spend. For example, if your business incurred £1m in qualifying spend, you would receive £200,000 in tax credit.

HMRC applies this credit against your Corporation Tax bill. If your bill exceeds the credit, HMRC deducts the difference, so you pay less. If your tax bill is smaller than the credit, or you’ve made a loss in the current tax year, HMRC pays you the remaining credit in cash.

The credit is taxable, so the amount you keep will be lower than the headline figure. After Corporation Tax, that 20% works out at roughly 15-16% of your qualifying spend, depending on your tax position. That means your credit would be worth nearer to £150,000-£162,000 using the example above.

You can find full details about the merged scheme and how to claim on the GOV.UK website.

Minimising idle cash

A successful R&D tax relief claim can reduce your tax burden – freeing up resources to reinvest in your business. But holding those funds in a current account, which typically offers little to no interest, could mean they lose value to inflation.

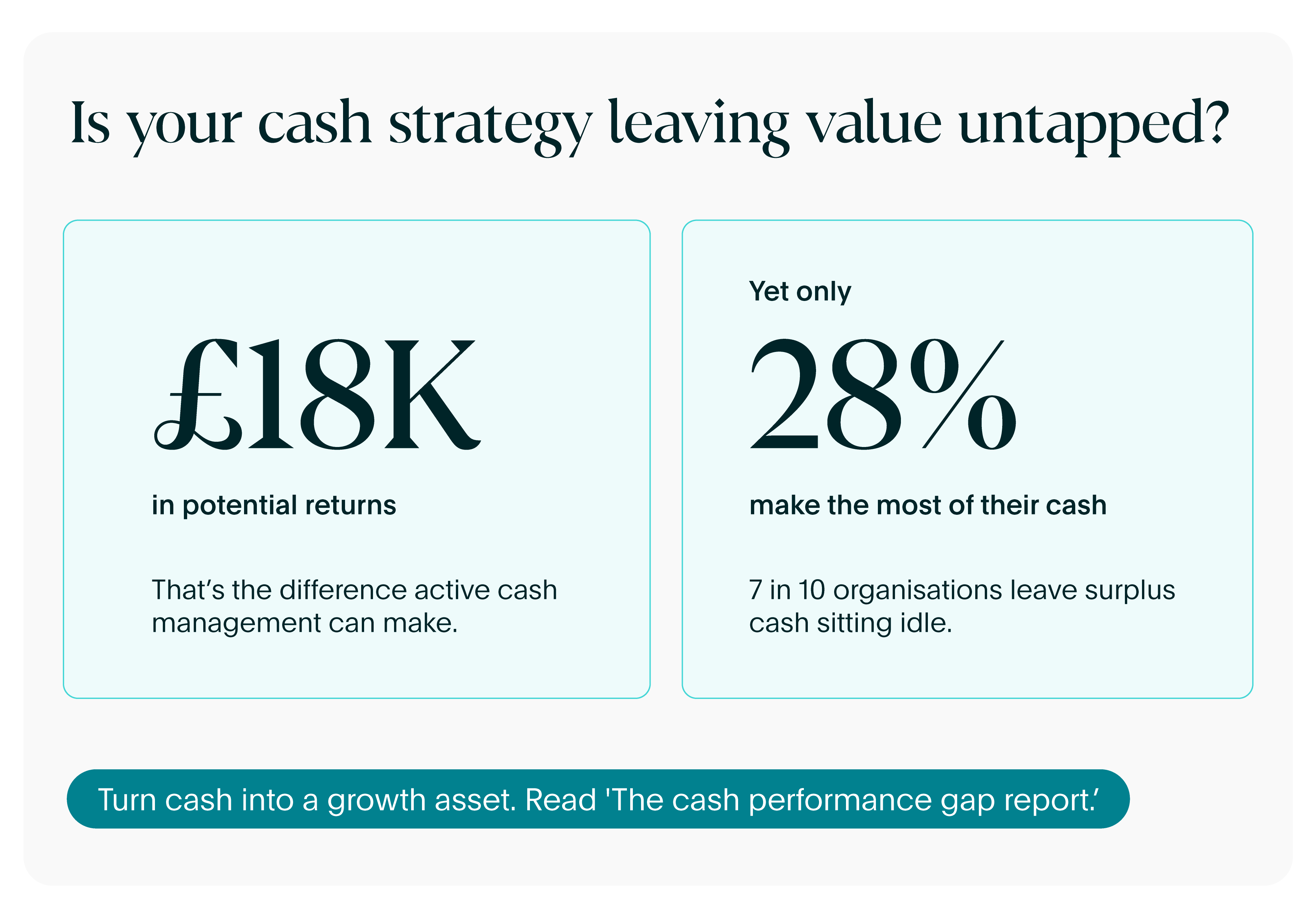

Our Cash Performance Gap Report shows 72% of UK SMEs leave their cash idle. For a business, that’s up to £18,000 a year in missed returns. Dividing capital between Instant Access and Fixed Rate business savings accounts can help you protect and grow your reserves.

Enhanced R&D Intensive Support

Enhanced R&D Intensive Support

Enhanced R&D Intensive Support provides more generous tax relief to loss-making SMEs that spend at least 30% of their costs on R&D. This typically includes early-stage businesses in industries like technology and software.

To qualify for ERIS, your business must have fewer than 500 employees, and either a turnover below €100m or a balance sheet under €86m. Your business must also be making a trading loss for tax purposes before any additional R&D tax deductions are applied.

If you qualify, HMRC lets you claim an additional deduction of 86% on your qualifying R&D costs. You can then surrender that loss to HMRC in exchange for a cash tax credit at a rate of 14.5%. In the best case, HMRC provides tax credits up to 27p for every £1 of qualifying R&D spend – but the actual amount depends on the size of your trading loss.

You can find out more about ERIS, the conditions for applying, and how to calculate the support available to you on the GOV.UK website.

Getting more from your cash credit

If you qualify for ERIS, your R&D tax credit could provide a meaningful cash injection which can cover the cost incurred while doing research or fund further innovation.

Holding that money in a business savings account can keep it secure and earning interest until you’re ready to use it.

A cash segmentation framework helps you allocate funds more deliberately. Dividing reserves into operational, buffer, and strategic tiers means you can earn higher returns while keeping funds accessible when it matters.

R&D tax relief FAQs

What is the 80% rule for R&D tax credits?

The 80% rule was a previous HMRC requirement for claiming employee salary costs under the R&D tax relief scheme. Under this rule, if an employee spent 80% or more of their time on research and development activities, the business could claim R&D tax credits for 100% of their salary.

HMRC has withdrawn this rule. Now, HMRC expects you to apportion staff costs in a simpler and fairer way – claiming the proportion of an employee’s working time spent on qualifying R&D. If someone’s entire role involves R&D, you can claim 100% of their employment costs.

How long does an R&D tax relief claim take?

HMRC aims to pay R&D tax credits promptly, but processing and approval can take up to 12 months.

Adjusting your business’s cash flow forecast to allow for potential delays could help you navigate unexpected costs and fund projects without disruption.

Do I need to tell HMRC before I claim?

If you’re claiming R&D tax relief for the first time, or haven’t claimed in the last three years, you’ll need to notify HMRC within six months of your accounting period ending.

You’ll also need to file an Additional Information Form before your Corporation Tax return for every claim.

Making the most of R&D tax relief

R&D tax relief provides innovative businesses with the opportunity to lower their Corporation Tax bill or receive a cash credit, freeing up cash to reinvest.

This extra capital base can help you grow your business and manage the risks associated with developing new products or technologies.

And that money doesn’t have to sit idle between projects. Our research shows 64% of UK SMEs hold surplus cash in current accounts offering low to zero returns.

High-interest business savings accounts could help you protect and grow your cash to manage uncertainty and scale up your operations.

Open high-interest business savings accounts with Flagstone

Build a portfolio that meets every business need, with Instant Access, Fixed Term, and Notice accounts.

With Flagstone, you can access hundreds of business savings accounts from 40+ FSCS-protected banks. All in one place, with one login, and a £100,000 minimum deposit.