Small business rate relief: at a glance

- What do I need to know? Small business rate relief could allow qualifying Small to Medium-Sized Enterprises (SMEs) to lower their tax bill.

- What does it mean for me? Even if your business property is valued above the small business rate relief threshold, you could still save on your tax bill through tapered relief, multipliers, and caps.

- Why does it matter? Paying less in tax could leave you with more cash to pay future bills, reinvest in growth, or absorb unexpected costs.

Government data shows that SMEs saved £2.1bn through small business rate relief in the 2024/25 tax year. This relief allows small businesses to reduce the tax they pay on their property by up to 100%. But how does it work?

In this guide, you'll learn whether your business is eligible for small business rate relief, how much you could get, and how to earn a better return on the money you save with high-interest business savings accounts.

What is small business rate relief?

The partial or total reduction in business rates, which is a tax charged on commercial properties.

Your local council calculates your business rates by multiplying your property’s ‘rateable value’ by a ‘multiplier’ for each tax year (more on this later). The rateable value is an estimate of the annual market rental value of your property. This value is determined by the Valuation Office Agency (VOA), and is not based on the rent you currently pay.

2026 rateable values

On 01 April 2026, the VOA introduced new rateable values based on market rental data from 2024. This means your property’s rateable value may have changed, and you may have to pay more or less tax as a result.

It’s important to regularly review your rateable value and business rates bill to check if you’re overpaying or if you’re entitled to additional relief. If you believe your rateable value is incorrect, you can challenge your business rates valuation with the VOA.

In England, the government sets small business rate relief at the following thresholds:

| Rateable property value | Tax relief |

| £12,000 or less | 100% |

| £12,001 to £15,000 | Tapered from 100% to 0% |

| £15,000+ | None |

How does tapered relief work?

Even if you don’t qualify for full small business rate relief, you could still save on business rates through tapered relief.

If your property’s rateable value is between £12,001 and £15,000, the amount of relief you can claim decreases gradually from 100% to 0%.

Below is an example of how tapered relief works for different rateable values:

| Rateable property value | Tax relief |

| £12,000 | 100% |

| £13,000 | 66.7% |

| £14,000 | 33.3% |

| £15,000 | None |

Properties with a rateable value over £15,000 do not qualify for small business rate relief. But you could still benefit from other reliefs, multipliers, and caps that reduce your bill (more on these later).

Small business rate relief outside of England

Small business rate relief differs slightly in Scotland, Wales, and Northern Ireland:

Scotland

In Scotland, the Small Business Bonus Scheme provides 100% tax relief on properties with a rateable value of up to £12,000. Tax relief then scales gradually from 100% to 0% for properties valued between £12,001 and £20,000.

Wales

The Welsh government offers 100% small business rates relief on properties with a rateable value of up to £6,000. Tapered relief is available for properties valued between £6,001 and £12,000.

Northern Ireland

In Northern Ireland, small business rate relief is based on the Net Annual Value (NAV) of your business property, rather than its rateable value.

You could get 50% tax relief on properties with an NAV of up to £2,000. Relief then drops to 25% for properties with an NAV between £2,001 and £5,000, and 20% for those with an NAV between £5,001 and £15,000.

Reducing your tax bill without small business rate relief

If you own or rent a business property with a rateable value over £15,000, the government still offers support to reduce your business rates bill.

Multipliers

The UK government uses multipliers to determine business rates. You can calculate your tax bill by taking your property’s rateable value and applying the corresponding multiplier.

Which multiplier applies to you depends on your rateable value and the type of business you run.

The multipliers for the 2026 to 2027 tax year* are:

| Rateable property value | Multiplier |

| £500,000+ | 50.8 pence |

| £51,000 to £499,999 | 48 pence |

| Below £51,000 | 43.2 pence |

*If you run a retail, hospitality, or leisure business, lower multipliers may apply.

The government applies its lowest 43.2 pence multiplier on properties with a rateable value below £51,000. If your rateable value has increased above the £15,000 small business rate relief threshold since April 2026, the lower multiplier could still help reduce your tax bill.

Transitional relief

Transitional relief limits how much your business rates bill can increase following a revaluation. So, even if your rateable value increases above the relief threshold, you're less likely to receive an unmanageable bill that could impact your cash flow.

These caps are scaled to the rateable value of the property. The table below shows the maximum annual increase allowed in the 2026 to 2027 tax year:

| Rateable property value | Percentage cap |

| Up to £20,000 (£28,000 in London) | 5% |

| £20,001 (£28,001 in London) to £100,000 | 15% |

| £100,000+ | 30% |

Your cap then increases gradually each year until 2029, giving you time to adjust to the higher costs.

Supporting small business relief

The government also offers another type of relief called ‘supporting small business relief’. This scheme caps business rates if your bill has risen due to a revaluation and you've lost some or all of your small business rate relief.

On 01 April 2026, the government updated the supporting small business relief scheme to reflect the VOA's new rateable values.

For the 2026 to 2027 tax year, your bill will increase by no more than £800 or the percentage caps below – whichever is greater.

| Rateable property value | Percentage cap |

| Up to £20,000 (£28,000 in London) | 5% |

| £20,001 (£28,001 in London) to £100,000 | 15% |

| £100,000+ | 30% |

Make more of your business cash

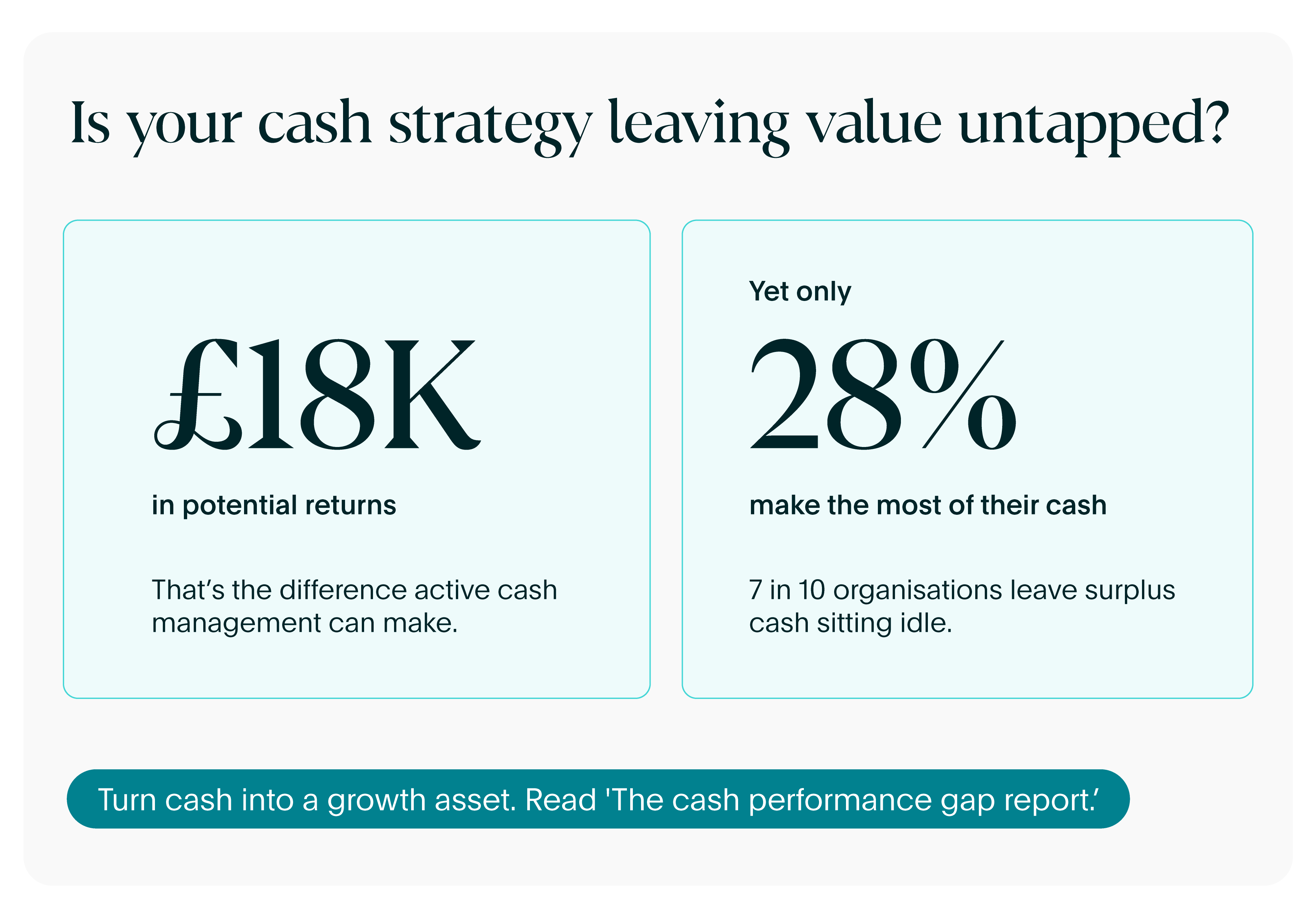

Small business rate relief could reduce your tax bill, leaving you with more cash to manage and grow your business. But what you do with that money matters. Our 'cash performance gap report' shows that 72% of organisations leave their cash idle. For the average SME, that's up to £18,000 a year in missed returns.

Holding your cash reserves in high-interest savings accounts means your cash earns interest while you keep it safe to one side for future tax bills, unexpected costs, or strategic initiatives. Strengthening cash reserves can be transformative for SMEs, as it gives CFOs and business owners greater flexibility to navigate financial risks, scale up during profitable periods, and invest in new business growth.

Balance growth and access

High-interest business savings accounts could help you increase earnings on your reserves, generating lower-risk returns rather than leaving cash sitting idle.

Cash flow forecasting allows you to confidently split liquid capital across instant access business savings accounts, business notice accounts, and fixed rate business savings accounts. So, you can maintain quick access to funds while earning higher returns on cash that’s not needed immediately.

Frequently asked questions about small business rate relief

Is small business rate relief ending?

The government has not announced plans to withdraw small business rate relief. Your eligibility for small business rate relief could end if your property is revalued above the current £15,000 threshold. But it’s important to check the details on the GOV.UK website.

What are the criteria for small business rate relief?

You can qualify for small business rate relief if you rent or own a business property with a rateable value up to £15,000. If your property is valued up to £12,000, you could qualify for 100% tax relief - with tapered relief then available between £12,001 and £15,000.

If your business occupies multiple properties, you might still qualify. But the additional properties must have a rateable value below £2,899, and the combined rateable value on all properties must not exceed £20,000.

What is the threshold for 100% business property relief after April 2026?

The threshold to qualify for 100% relief is £12,000. This threshold has been in place since April 2017.

How do I apply for small business rate relief?

To apply for small business rate relief, the government advises contacting your local council to check your eligibility.

Boost growth and resilience with small business rate relief

Understanding how you could reduce your tax bill could make your business more agile. A lower tax bill means more money to put back into your business, giving you the flexibility to pursue valuable opportunities and build resilience against unexpected costs.

Savings platforms like Flagstone give you the flexibility to grow and protect your capital, whether you prioritise instant access or the higher interest rates that are typically available with notice or fixed-rate accounts.

Earn more on your business cash reserves with Flagstone

Flagstone offers access to hundreds of business savings accounts from 40+ FSCS-protected banks. All in one place, with one login, and a £100,000 minimum deposit.