Last updated: 19 August 2025

Understanding economic factors can help you make more informed financial decisions to grow and protect your wealth. In this article, you'll learn some of the key economic elements that can influence the growth of your savings.

The impact of economic factors: at a glance

- Inflation is when the prices for goods and services increases. How quickly they rise is called the inflation rate.

- The Bank of England aims to keep inflation at 2%, so price rises remain low and steady.

- The Consumer Price Index (CPI) tracks the price of a ‘basket’ of over 700 goods and services each month to measure inflation.

- The Bank of England base rate is the UK’s main interest rate, which influences the rates banks offer on savings accounts.

- Gross Domestic Product (GDP) shows the total value of all goods and services the UK produces in a set period.

What is inflation?

The term ‘inflation’ refers to the increase in the price of goods and services in the UK. How quickly prices go up is called the inflation rate. When economists talk about inflation, they express it as a percentage change over a year. For example, if inflation in the UK is 3%, it means that, on average, prices are 3% higher than they were the same time last year.

High inflation means prices are increasing swiftly, which reduces purchasing power over time. So the money you have today doesn't buy as much as it used to. If wages don't keep up with these rising prices, people's standards of living can fall. Additionally, if the inflation rate rises too high, it can contribute to a recession.

Low inflation means prices are increasing slowly. It's beneficial for consumers because your money keeps its real value, meaning it goes further. But if inflation is too low (below the government's 2% target), it can mean there's not enough demand for goods and services. This isn't good for businesses, and can lead to job losses.

Keeping a low and stable level of inflation creates a healthy economy. The government sets an inflation target, which the Bank of England is responsible for maintaining.

How is inflation calculated?

The Office for National Statistics (ONS) is responsible for checking how much prices have risen in the UK. They track the expenses of over 700 commonly bought items, ranging from basic necessities like food and transport costs, to larger purchases like cars and holidays. The total cost of this ‘basket’ of items reflects the overall change in prices. This is known as the Consumer Price Index (CPI).

To calculate the inflation rate, the ONS compares the current cost of the basket to what it cost a year ago. The change in price over that year tells us the inflation rate. The ONS run a large number of surveys to ensure the index accurately reflects what consumers are buying, and that the prices are correct.

Each month, the ONS shares the latest CPI data on their release calendar.

You can use the ONS’s inflation calculator to see how prices have changed over time.

Why does the inflation rate matter for savers?

The inflation rate is important for savers who are looking to grow their wealth. Here’s why it matters and how it can impact your saving strategy.

1. It influences the base rate

The Bank of England adjusts the base rate to control inflation, using the CPI (the ‘basket’ of goods we mentioned earlier) as a key indicator for measuring inflation. Higher inflation may prompt the Bank to raise the base rate – the single most important interest rate in the UK. This often leads to higher returns on savings accounts, as banks pass on the increased rates to savers.

But if the base rate doesn’t keep pace with inflation, you may experience a decrease in the real value of your savings.

One way to shield your savings from the negative effects of inflation is by proactively reviewing the interest rates on your savings accounts. If your money is languishing in a low-interest account, especially one earning less than inflation, consider exploring other options.

2. It affects retirement planning

Many retirees live on fixed incomes from pensions, savings, or annuities. An annuity is a financial product that guarantees a lifetime income in return for a lump sum payment.

Any increase in the cost of living due to inflation can reduce the purchasing power of your income over time. Understanding CPI trends can help you adjust your retirement savings strategy to stay financially secure later in life.

Certain pension plans offer cost-of-living adjustment, ensuring you’re protected against fluctuations in inflation. To minimise a drop in the real value of your pension pot, consider talking to a Financial Adviser who can provide tailored advice based on the latest economic conditions.

3. It affects purchasing power

£1 is essentially worth less if, overall, prices for goods and services increase. Remember how much you were able to buy for £1 years ago – much more than you’re able to buy today. This is due to inflation. If the interest rate on your savings account is lower than the inflation rate, your money’s purchasing power decreases over time.

What is the Bank of England base rate?

The Bank of England base rate (also known as Bank Rate) is the main interest rate in the UK. It’s set by the Monetary Policy Committee (MPC) who collectively decide the base rate as part of their efforts to meet the government's inflation 2% target.

It’s important because it sets the interest rate for commercial banks. This affects the rates that banks charge you for loans and the interest you earn on your savings.

To prevent prices rising too quickly, the Bank adjusts the base rate. When rates rise, borrowing becomes more expensive, so people tend to spend less and save more. This decline in spending can help slow down price increases.

How is the base rate decided?

The MPC is made up of nine members, each with expertise in economics and monetary policy. At each meeting, the Governor of the Bank of England proposes a policy they believe will secure majority support from the MPC members, who then vote on it. Each member's vote is independent. In case of a tie, the Governor has the deciding vote.

The decision-making process happens every six weeks, and the MPC announces its decision publicly at noon on Thursdays.

You can view the dates for upcoming announcements on the Bank of England website.

Why does the base rate matter to savers?

Interest rates on savings accounts tend to be linked to the Bank of England base rate. When the base rate rises, banks often offer higher interest rates to attract customers.

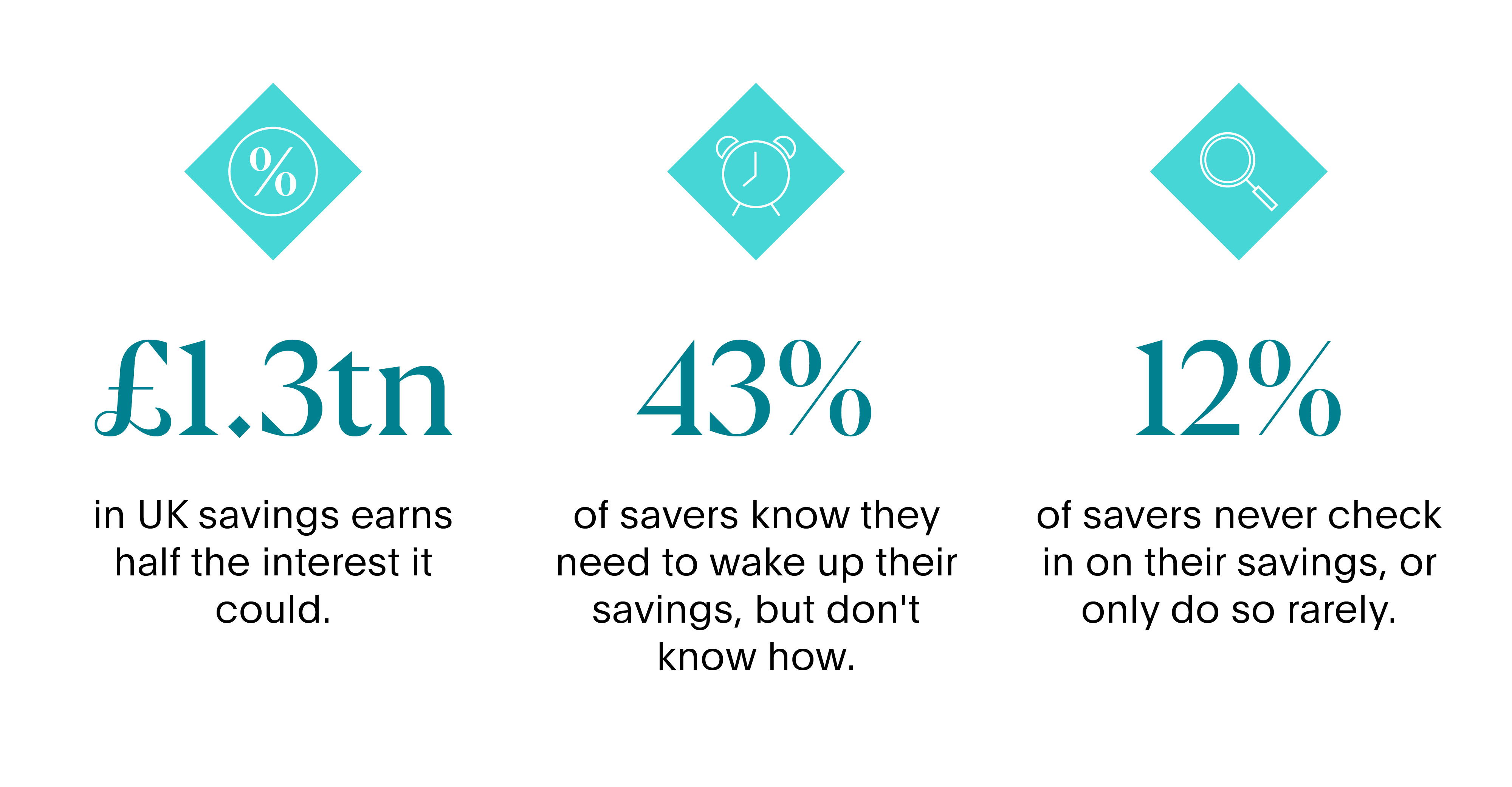

Despite the competitive rates on offer across the market, over £1tn in UK savings is still languishing in low-interest accounts – earning less than the rate of inflation.

Loyalty to old accounts often doesn’t pay off. Most high street banks offer some of the lowest interest rates on standard savings accounts. That means your money is benefitting them more than you. If your cash isn’t reaching its full potential, it’s worth exploring options that provide higher interest to grow your money.

What is Gross Domestic Product?

Gross Domestic Product (GDP) measures the value of goods and services produced in a country over a period of time. It serves as an indicator of the size, growth, and overall health of the economy, allowing for comparisons with different economies at different points in time.

How is GDP calculated?

The ONS calculates GDP by meticulously gathering data from companies across the UK. It uses three primary methods:

- the output approach – this sums up the total value of goods and services produced

- the income approach – this sums up everyone's income within the country

- the expenditure approach – this considers all the money spent

Using this data, the ONS produces the official GDP figure for the UK.

This figure serves as an indicator of the country's economic health, guiding policymakers, businesses, and investors in their decision making.

The ONS provide updates on GDP numbers every month, with bigger updates each quarter.

Why does GDP matter to savers?

GDP growth plays a significant role in shaping the economic landscape and consequently affects savers in various ways.

1. GDP growth can influence the base rate

When the Bank of England raises the base rate during periods of economic growth, banks and financial institutions often pass on these higher rates to customers. As a result, you can benefit from higher interest rates on your savings accounts.

2. GDP growth can lead to inflation

When GDP is growing, it often leads to increased consumer spending and demand for goods and services. This heightened demand can push prices higher, leading to inflation. When this happens, it’s important to be mindful of the impact of inflation on your savings. Many savers choose accounts with higher interest rates to help their money hold its value when prices rise.

Are you using interest rates to your advantage?

Take a look at your existing accounts. If your cash is sitting idle in a current account for convenience, you could be missing out.

With Flagstone, you get access to exclusive rates from over 65 banks – all on one secure platform, with one password.

Discover how you could protect and grow your cash.