Fixed-rate business savings accounts: at a glance

- What do I need to know? Fixed-rate business savings accounts offer a guaranteed interest rate over a set term, but funds are locked in until maturity.

- What does it mean for me? In exchange for limited access, you can benefit from predictable growth and often higher interest rates.

- Why does it matter? If your business has surplus cash that is not needed immediately, you can grow it safely while knowing exactly what you’ll earn in interest.

Fixed-rate business savings accounts let you lock money away for a set period in return for a guaranteed interest rate.

By keeping funds untouched, businesses can earn predictable, often higher, interest rates. This makes fixed-rate business accounts increasingly attractive to finance leaders seeking a relatively low-risk way to grow large cash reserves.

But is the trade-off between higher interest rates and limited access always worth it?

In this article, you’ll learn how fixed-rate business savings accounts work, their benefits and limitations, and whether they fit your cash strategy.

Are fixed-rate accounts worth it for your organisation?

Fixed-rate business savings accounts are a strong choice for businesses who hold surplus cash they don’t need immediately and want predictable growth. Fixed-rate accounts are also sometimes called fixed terms or bonds.

They tend to deliver the most value when your company has significant reserves, stable cash flow, or specific savings goals in mind.

These could include planned expenses like equipment purchases or facility upgrades. If you know a major cost is coming up, you can save your funds in a fixed-rate account and earn higher interest in the meantime.

Upcoming tax liabilities are another common use case for fixed-rate business accounts. If you’re setting aside funds for a corporation tax bill due at the end of the financial year, a fixed-rate account lets you earn a predictable return until your payment is due.

Finally, if you have money earmarked for a strategic goal, a fixed-rate account can be a great option to grow your funds while keeping them secure until you need them. This might include an acquisition, market expansion, or a specific project such as a new product launch.

How do Fixed-Rate business savings accounts work?

With a fixed-rate business savings account you usually get a higher interest rate in exchange for locking away your cash for a set period, normally ranging from six months to five years.

Once you open the account, you won’t be able to access your money for the duration of the term without incurring penalties. During this period, you’re typically paid interest on your cash deposits monthly or annually, depending on the terms of the account you opened.

When the term ends, you can choose to withdraw your deposit and interest, reinvest your cash into another business savings account, or opt for a laddering approach. This involves spreading your funds across multiple accounts that mature at different times.

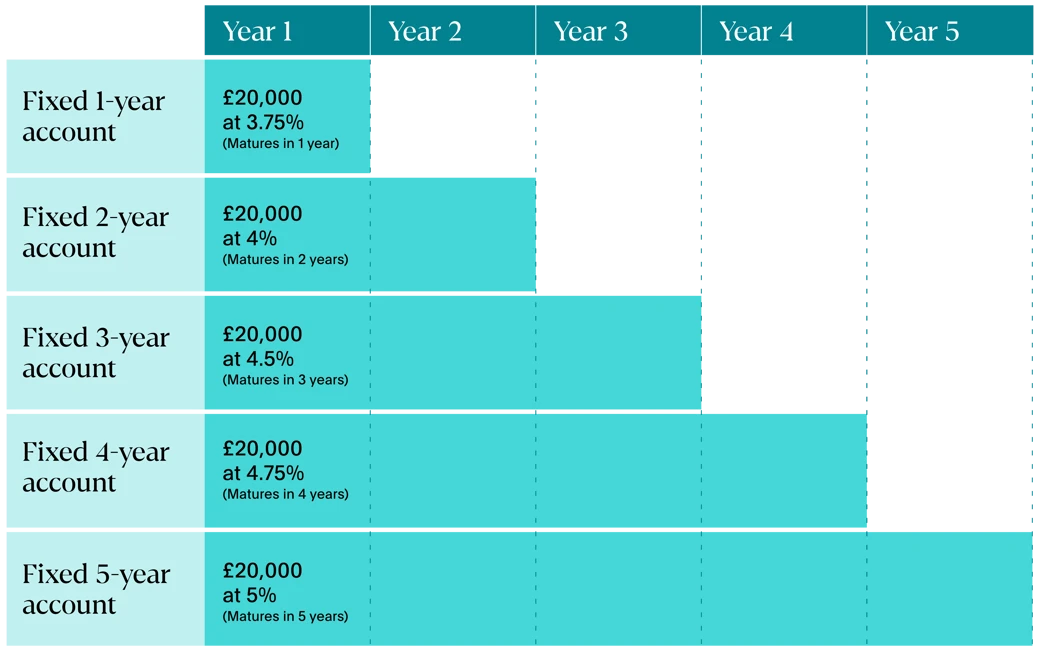

Here’s an example of how investing £100,000 could work over five years:

What are the benefits of fixed-rate business savings accounts?

Fixed-rate savings accounts offer many advantages for organisations, including:

Higher interest rates

Because your money is locked in, fixed-rate accounts usually pay higher interest rates than instant access business savings accounts. Depending on the provider, longer terms may also offer higher interest rates.

Predictable returns

Your interest rate remains unchanged for the full term, protecting your funds from base rate fluctuations and giving you full visibility over your expected returns.

Low-risk growth for large deposits

You can open multiple fixed-term savings accounts and spread deposits across different banks, interest rates, and maturities. This helps optimise returns while keeping eligible funds within the Financial Services Compensation Scheme (FSCS) protection limits.

With a savings platform like Flagstone, you can open multiple Fixed-Rate business savings accounts with one application and manage them all in one place, with a single password.

What to consider before locking away your funds

Before you decide if a fixed-term account is a good option for your business, it’s worth looking at some of the possible downsides:

Limited access

Most fixed-rate accounts require you to leave your money untouched for the full term. Early withdrawals can often lead to penalties or loss of your interest earnings.

Lack of flexibility if rates rise

If the base rate increases during your fixed term, your return won’t increase. This could mean you end up earning less than current market rates.

Minimum deposit

Most providers will ask for a minimum deposit to open an account. This needs to be paid in a single lump sum, so you’ll need to ensure the full amount is available.

How do fixed-rate accounts compare to other business savings options?

Businesses have a range of savings options available. And they each offer different levels of access, commitment, and possible returns. See how fixed-rate accounts compare:

| Instant access accounts | Notice accounts | Fixed-rate accounts |

| Unlimited withdrawals at any time. | Require advance notice to withdraw your funds. | Funds are locked in until the end of the term. |

| Variable rates - typically lower than other savings options. | Variable rates - usually higher than instant access accounts. | Fixed rates - often higher than instant access and notice accounts. |

| Low risk. FSCS protected*. | Low risk. FSCS protected*. | Low risk. FSCS protected*. |

| Ideal for businesses who need maximum flexibility and immediate access to their funds. | A smart choice for those who can plan withdrawals in advance and want competitive interest rates with some flexibility. | Best for companies looking for predictable, higher interest rates, who don’t need access to their money right away. |

* FSCS protection applies for eligible deposits up to £120,000 per person, per authorised institution.

Predictable growth for your business cash

A fixed-term business savings account lets you grow your cash reserves with a reliable return. If stability and predictable growth are your priorities, these accounts can be a smart addition to your portfolio.

While you do restrict access to your cash, you gain the clarity and certainty needed to manage large sums securely, helping you to plan ahead with confidence.

Open Fixed-Term business savings accounts with Flagstone

Access hundreds of Fixed-Rate accounts and lock in your interest from start to finish.

All in one place, with one application, and a minimum deposit of £100,000.